Federal Budget: What it means for you

Workers, small business owners, first home buyers and rugby league players in Papua New Guinea are among the winners of this year’s historic Federal Budget, however, Baby Boomers, wealthy families and property investors are among the losers with Treasurer Jim Chalmers announcing major changes to negative gearing, capital gains tax and discretionary trusts on Tuesday night.

This summary provides a high-level look at key measures in the Albanese Government’s fifth Budget and what they mean for you.

The centerpiece of Tuesday night’s Federal Budget are proposals to limit capital gains tax (CGT) discounts and negative gearing on property investments, and the introduction of a permanent $250 Working Australians Tax Offset (WATO) in a bid to improve housing affordability and “rebalance a system which is more generous to assets than it is to labour”.

From 1 July 2027, the Government plans to scrap the 50% CGT discount on assets held for more than 12 months, a benefit introduced in 1999. Instead, the CGT will return to the pre-1999 policy of taxing inflation indexed gains, with a 30% minimum tax applied on net capital gains. This will apply to all assets including real estate.

Negative gearing, which allows investment losses to be offset against taxable income, will be limited to newly built homes to support new housing supply. Existing residential property owned at the time of the Budget announcement will be carved out from this change. Commercial property and other assets (e.g. shares) will remain subject to existing arrangements.

The tax changes will be partially offset by the WATO that around 13 million workers will be able to claim in tax returns from the 2027-28 financial year.

The Budget also confirmed a new $1,000 instant tax deduction, allowing eligible taxpayers to claim a flat deduction of $1,000 on work related expenses, starting from July 1, 2026. These initiatives are on top of already legislated tax cuts to deliver up to $536 in annual savings for taxpayers and aim to provide some cost-of-living relief.

Inflation and interest rate hikes

Tuesday night’s Budget comes during a period of economic and geopolitical uncertainty, with open conflicts around the world impacting global supply chains and energy costs.

Inflation is forecast to hit 5% in June, adding to cost-of-living pressures and increasing the probability of further interest rate hikes.

Despite the challenging economic environment, the Government’s Budget bottom line improves due to significant savings from an overhaul of the National Disability Insurance Scheme (NDIS), worth more than $35 billion over four years. Tax reforms will also save the Government $3.5 billion over the same period.

Superannuation gets a break

Superannuation hardly got a mention on Budget night and is carved out of proposed changes.

This is a welcome change, after the 2023-24 Budget which contained the Government’s Building a stronger and fairer super system reforms including the controversial Division 296 tax.

Key measures

This summary focuses on key measures contained in the Budget, based on the limited details provided in the Budget papers and accompanying fact sheets.

Importantly, these proposals require the passage of legislation before they are implemented (unless noted otherwise).

We will continue to monitor these proposals and issue further communications as more details emerge.

Taxation – Personal

Capital gains tax (CGT) reform Proposed effective date: 1 July 2027

From 1 July 2027, the 50% CGT discount will be replaced by cost base indexation for assets held for more than 12 months, with a 30% minimum tax on net capital gains. These changes will apply to all CGT assets (including property, shares and pre-20 September 1985 CGT assets), held by individuals, trusts and partnerships. Indexation will be calculated using Consumer Price Index (CPI) in a similar manner to arrangements previously in place between 1985 and 1999.

A minimum tax rate of 30% will apply to real capital gains accruing from 1 July 2027 (with no impact until the income is realised). The minimum tax rate is to reduce the benefit of taxpayers deferring capital gains realisation to years where their marginal tax rates are low. Recipients of means-tested income support payments, such as the Age Pension or JobSeeker, will be exempt from the minimum tax if they receive any payment in the financial year in which they realise the capital gains.

Transitional arrangements will limit the impact on existing investments by ensuring the changes only apply to gains arising on or after 1 July 2027. The 50% CGT discount will continue to apply to gains arising before 1 July 2027. Capital gains on pre-20 September 1985 assets arising before 1 July 2027 will remain exempt from CGT.

For assets owned prior to 1 July 2027 and sold after 1 July 2027, taxpayers must either:

Seek a valuation of the asset as at 1 July 2027, which will include using quoted prices for assets such as shares; or

Use a specified apportionment formula that estimates the asset’s value on 1 July 2027, based on its growth rate over the asset’s holding period. The Government has indicated that the ATO will develop tools to help taxpayers estimate this value.

Investors of new residential properties will be able to choose either the 50% CGT discount, or cost base indexation and the minimum 30% tax when they sell the property.

Restricting negative gearing to new builds Proposed effective date: 1 July 2027

From 1 July 2027, losses related to existing residential investment properties purchased from 7:30pm AEST 12 May 2026 will only be deductible against other income from residential properties, including capital gains. When an investor has excess losses, they will be able to carry forward these losses to offset against residential property income in future years.

These changes will apply to individuals, partnership, companies, and most trusts. Widely held trusts (for example, most managed investment trusts) and superannuation funds (including SMSFs) will be excluded.

Changes to negative gearing will only apply to residential property. Commercial property and other asset classes, such as shares, will remain subject to existing arrangements.

Newly built residential properties can continue to be negatively geared before and after 1 July 2027.

Transitional arrangements

For established residential properties:

Properties held at the time of the Budget announcement will be allowed to be negatively geared in future years until sold.

Properties purchased between Budget announcement and 30 June 2027 may be negatively geared during this period, but not from 1 July 2027.

A 30% minimum tax rate on discretionary trusts Proposed effective date: 1 July 2028

From 1 July 2028, the Government will introduce a minimum tax on discretionary trusts, requiring trustees to pay tax at a minimum rate of 30% on the taxable income of the trust. Beneficiaries, other than corporate beneficiaries, will receive non-refundable credits for the tax payable by the trustee.

There are some exclusions including fixed testamentary trusts, complying superannuation funds and charitable trusts

Recipients of means-tested income support payments, such as the Age Pension or JobSeeker, will be exempted from the minimum tax if they receive any payment in the financial year in which they realise the capital gain.

Rollover relief

Expanded rollover relief will be provided for three years from 1 July 2027 to support small businesses and others that wish to restructure out of discretionary trusts into another entity type.

Instant tax deduction Proposed effective date: 1 July 2026

As announced ahead of Budget night, tax residents who derive assessable labour income can claim a standard deduction of up to $1,000 for work-related expenses in their 2026–27 income tax return, without the need for receipts.

The standard deduction is reduced, dollar-for dollar, by general and specified work-related expense deductions claimed (such as certain transport, car, repair, capital allowance and COVID-19 test deductions) so that individuals do not receive a double benefit.

Certain deductions would remain available in addition to the standard deduction, including deductions that are not in connection with earning assessable labour income (such as investment expenses), income protection insurance premiums, charitable donations, costs of managing tax affairs, payments for membership of a union or other trade, business or professional association.

Individuals who incur more than $1,000 of work-related expenses can elect to claim their actual deductions under existing rules instead.

Introducing the Working Australians Tax Offset Proposed effective date: 1 July 2027

A Working Australians Tax Offset (WATO) will be introduced to provide a permanent annual tax offset for individuals for income derived from work, such as wages and salaries and the business income of sole traders.

The WATO will increase the effective tax-free threshold for income derived from work by nearly $1,800 to $19,985 (or up to $24,985 for those eligible for the Low Income Tax Offset).

This measure is in addition to the legislated tax cuts due to take effect on 1 July 2026 (reduction of the 16% marginal tax rate to 15% on taxable income between $18,201 and $45,000) and 1 July 2027 (a further reduction of the tax rate to 14%).

Fuel Resilience Package

The Budget contains a $14.8 billion Strengthening Australia’s Fuel Resilience Package that aims to secure fuel and fertiliser immediately, build up reserves for the future and relieve immediate pressure on fuel users.

So far from March to June, the government has secured more than a billion extra litres of fuel and it is establishing a $3.2 billion government-controlled Australian Fuel Security Reserve, which will hold around 1 billion litres of diesel and jet fuel to provide an additional buffer during any future crisis. To help keep trucks, trains and planes moving, manufacturing and logistics businesses may be eligible for interest-free loans from the National Reconstruction Fund’s (NRF) $1 billion Economic Resilience Program.

Aged Care

Extra funding for residential aged care Proposed effective date: From 1 January 2027

The Government will fund an additional 5,000 aged care beds each year, principally for individuals with limited financial means, through new subsidies designed to incentivise aged care providers from 1 January 2027:

Newly constructed aged care homes will receive a New Home Payment of $30 per supported resident per day.

Existing homes that undergo significant expansions (i.e. increasing the number of beds by 40% or more) will receive a Significant Improvement Payment of $15 per supported resident per day.

Accommodation supplements payable to residential care providers will also increase from 2027, with additional top-ups from 2028 for aged care homes with more than 60% supported residents, subject to finalising implementation details.

Other changes

Changes to accommodation pricing, including replacing the maximum interest rate with an alternative way to convert a daily payment into a refundable deposit.

Improving consumer understanding and protections by giving individuals and providers clearer information about accommodation arrangements.

To support older people suffering from dementia, the government will invest $200 million for 20 additional Specialist Dementia Care Program units and an expansion of the Hospital to Aged Care Dementia Support Program.

Improving affordability and access to the Support at Home program Effective date: 1 October 2026

From 1 October 2026, personal care for Support at Home participants will be partially funded.

Personal care services (including showering, dressing and non-clinical continence management) will move from the Independence category to the Clinical Supports category. This means that participants with personal care services approved as part of their support plan and who have available Support at Home funding will be able to receive personal care services with no out-of-pocket cost, regardless of means.

Additionally, the Government will implement Support at Home program refinements, including improvements to assessments for faster access to places, digitising and simplifying the hardship application process and extending funding under the end-of-life pathway to provide more care for palliative patients, as well as bringing forward the release of Support at Home program places in 2026/27.

PBS changes for medicine affordability

New medicines will be added to Pharmaceutical Benefits Scheme (PBS) including treatments for cystic fibrosis, chronic kidney disease and various cancers. This includes permanently cutting the cost of COVID-19 oral antiviral medicines.

Other changes include capping the maximum cost of a general PBS prescription to $25 from $31.60, capping the general patient co-payment for PBS medicines at $25 per prescription and freezing concessional co-payments at $7.70 until 2030.

The Government is also providing $449.3 million to list the respiratory syncytial virus (RSV) vaccine Arexvy® for eligible older Australians on the National Immunisation Program to protect against respiratory infection caused by RSV.

Social Security

Changes to Pension Supplement to recipients overseas Proposed effective date: 20 September 2026

Currently, the Pension Supplement reduces from the full rate to the basic amount (payable indefinitely):

After six weeks if a recipient is temporarily overseas, or

Immediately if the recipient’s departure is permanent.

It is proposed that the full rate of payment is extended to 12 weeks for temporary departures before ceasing entirely, and for permanent departures, the Pension Supplement will cease entirely upon departure.

Reforming the National Disability Insurance Scheme (NDIS) Proposed effective date: From May 2026 onwards

Changes to the NDIS aim to deliver overall savings of more than $36 billion across the next four years. This will be achieved via a timeline of various changes for participants and providers.

These aim to return the scheme to its original intent of supporting Australians with significant and permanent disability while securing the NDIS for future generations

Other Measures

Reduction to Fringe Benefits Tax (FBT) exemption for electric vehicles (EVs) Proposed effective date: From 1 April 2027

The current full FBT exemption on EVs will transition to a 25 per cent discount with the change being phased in over three stages:

Under phase 1, the current EV FBT discount will continue in full until 31 March 2027.

Under phase 2 (1 April 2027 to 31 March 2029), the full FBT discount will apply only to EVs costing $75,000 or less, while EVs costing more than $75,000 but below the luxury car tax threshold (currently $91,387) will receive a 25% discount on payable FBT.

Under phase 3 (1 April 2029 onwards), all EVs below the luxury car tax threshold will receive a 25% discount on payable FBT.

Existing leases will not be impacted by these changes.

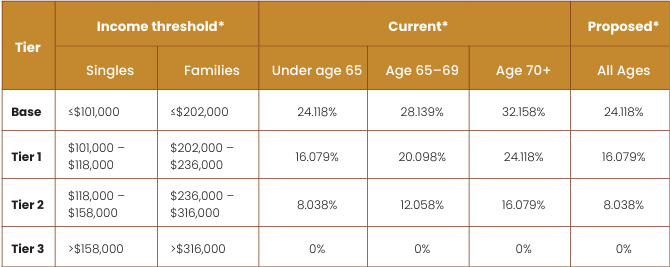

Removal of higher private health insurance premium rebate for older Australians Proposed effective date: 1 April 2027

The higher private health insurance rebate rates that currently apply for older Australians will be removed, so that rebate percentages for people aged 65 and over are aligned to the rates that apply to those under 65 on the same income tier.

Private health insurance rebate rates – current and propose

* Income thresholds and rebate rates are subject to change

Taxation – Businesses

Retaining the small business instant write-off permanently Proposed effective date: 1 July 2026

The Government will make the small business instant asset write-off permanent.

All other eligibility settings and mechanics remain unchanged. This means that small businesses, with aggregated annual turnover of less than $10 million, will be able to immediately deduct the full cost of eligible assets costing less than $20,000 that are first used or installed ready for use in the relevant income year.

The $20,000 threshold will apply on a per asset basis, so small businesses can instantly write off multiple assets. Assets valued at $20,000 or more (which cannot be immediately deducted) can continue to be placed into the small business simplified depreciation pool.

Reforming the treatment of company tax losses Proposed effective date: 1 July 2026 and 1 July 2028 respectively

From 1 July 2026, companies with annual turnover of less than $1 billion will be able to carry back a tax loss and offset it against tax paid up to two years earlier. Loss carry back will apply to revenue losses only and will be limited by a company’s franking account balance.

From 1 July 2028, loss refundability for small startup companies will also be introduced, allowing startups with aggregated annual turnover of less than $10 million that generate a tax loss in their first two years of operation to utilise the loss to generate a refundable tax offset. The offset will be limited to the value of fringe benefits tax and withholding tax on wages paid in respect of Australian employees in the loss year.

These changes aim to provide tax relief to businesses and startup companies

IMPORTANT INFORMATION

This publication is prepared by Personal Financial Services ABN 26 098 725 145, AFSL 234459 (“Licensee”). The information in this publication is general only and has not been tailored to individual circumstances. Before acting on this publication, you should assess your own circumstances or seek personal advice from a licensed financial adviser. This publication is current as at the date of issue but may be subject to change or be superseded by future publications. While it is believed that the information is accurate and reliable, the accuracy of that information is not guaranteed in any way. Past performance is not a reliable indicator of future performance, and it should not be relied on for any investment decision. Whilst care has been taken in preparing the content, no liability is accepted by the Licensee nor any of its agents, employees or related bodies corporate for any errors or omissions in this publication, and/or losses or liabilities arising from any reliance on this document. This publication is not available for distribution outside Australia and may not be passed on to any third person without the prior written consent of the Licensee. The information provided is current as at 12 May 2026 and is subject to change